EMT Practice Test

1. Question Content...

Question8: Which of the following is not a direct benefit of control self-assessment (CSA)?

Question12: The scope of a business process review primarily involves:

Question23: Which of the following is not an outcome of control self-assessment?

Question24: Which of the following is a preventive control strategy against fraud?

Question38: When interrogating an individual who is suspected of fraud, it is appropriate to:

Question40: A limitation of using ratio analysis in an audit engagement is that it:

Question45: Which of the following examples of audit evidence is the most persuasive?

Question47: Which of the following is a red flag associated with fictitious revenues?

Question52: Which of the following statements describes an engagement planning best practice?

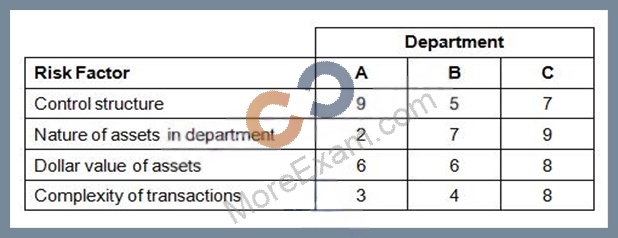

Question56: The best method for assessing the relative importance of risk factors is to:

Question59: The scope of a consulting engagement performed by internal auditors should:

Question88: All of the following tools are employed to control large-scale projects except:

Question129: When approving the final engagement report, which of the following is most critical?

Question141: Audit supervision includes approval of the engagement report in order to ensure that:

Question144: Which of the following would be an appropriate role of the internal audit function?

Question163: A post-audit questionnaire sent to audit clients is an effective mechanism for:

Question170: Which of the following actions is related to the preliminary survey process?